Purchasing a house is a fascinating time with regards to everyone's life. While you're getting ready to buy a house, there are several things you should know, one of which is your FICO rating. FICO appraisals are used to assess a singular's capacity to repay a credit. It's a three not entirely settled by the country's credit divisions using customer data from clients and moneylenders. It is settled using limits like as advance reward history, the length of current credit, and so forth. The monetary evaluation changes from 300 to 900 spots.

What is a Credit Score?

A FICO evaluation implies that the monetary sufficiency of an individual. This score relies upon information from a credit report, which joins portion history and outstanding commitment. The score goes from 300 to 850. A score of 700 or higher is seen as a fair score.

Sum does a FICO evaluation's expectation's?

If you are planning to buy a home or vehicle, you will require a fair FICO evaluation. If you don't have a fair FICO rating you can find it hard to get the credit you truly care about. What sum do you genuinely ought to have the choice to get embraced for a credit?

What Is a Conventional Mortgage?

A standard home advance is one of the most renowned home credit types. Thusly, customary home credits as often as possible have a lot of misguided judgments around them. The planned activities of a standard home advance is clear and banks will look at two essential components while choosing your capability.

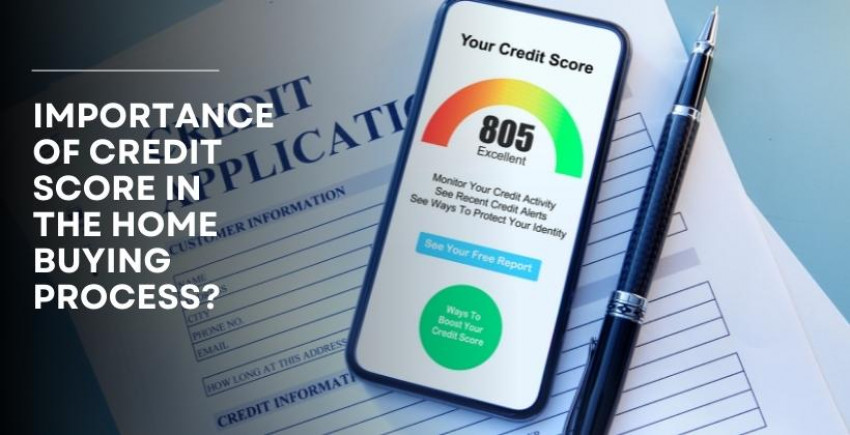

At any rate, how does your monetary evaluation impact the home-buying process?

Banks will check your FICO rating when you apply for a house advance to check whether you are a strong borrower. A FICO evaluation of 750 to 900 is regarded extraordinary and can give you various benefits, for instance, speedier credit supports, lower funding costs, and so on. Along these lines, before you apply for a home development, be sure you have a fair monetary appraisal. Your FICO evaluations will increase expecting you cover your Visa bills and MIs on time.

Underwriting of advances: Your monetary appraisal may similarly accept a section in getting a credit upheld. Getting a home development generally requires a FICO appraisal of some place in the scope of 620 and 650. In case your score isn't satisfactory, you should chat with your bank to figure out a good method for raising it.

• How might I dissect the best private credit offers?

While differentiating individual development offers, there are two or three things that ought to be considered before the application can be made. Individual advances are not the same in any case, yet they will be introduced by different banks and financial associations. These associations look at different principles to sort out who gets the development and how much interest they charge. Knowing what to look for and how to differentiate offers will help you with seek after the decision.

Advance Amount: If you have a low FICO rating, the credit aggregate you get will most likely be not actually the total you referenced. Accepting that you need a Rs. 30 lakh house advance, for example, your monetary appraisal could hold the bank back from supporting this total. Along these lines, you should have a go at a higher FICO rating to be equipped for a greater development aggregate.

Extended front and center portion: A lower FICO rating can achieve a higher beginning venture aggregate while purchasing a home. This is to ensure that the buyer is centered around repaying the commitment. For example, in case the standard introductory portion is 10% of the total aggregate, the advance expert could anticipate that you should pay 20%.

We really need to accept that you presently have a prevalent appreciation of monetary evaluations and what they mean for house purchases. As of late communicated, a higher FICO appraisal will achieve genuinely captivating credit offers, lower funding costs, longer repayment plans, and more important development aggregates. Accepting that your FICO rating is poor, ponder making all of your portions on time for the accompanying two or three months to raise it. It's similarly basic to look out for your score to check whether it's moving along.

source from:- navimumbaihouses